Acting as an “Atlas” for Our Western Companies in the Middle East

From meeting Ray Dalio to H.R.H. Princess Reema Bint Bandar Al Saud (Saudi Ambassador to the US), we witnessed first hand the effectiveness of aligning our investments with public industrial capital deployments as we supported our nuclear portfolio company, Transmutex, in forging relationships in the Middle East.

Investing in the Tailwinds of Public-Private Partnerships

Saudi Arabia plans to spend another $3.2T diversifying its economy away from oil by investing in the onshoring of existing and novel industrial technologies. Industrial-focused venture investors can capitalize on this large tailwind to build first of a kind facilities faster than ever before but it requires boots on the ground relationship building.

— Fund Developments —

Acting as an “Atlas” for Our Western Companies in the Middle East

The name of the fund makes clear our purpose. “Steel” has been the foundation of industrialization and we plan to invest in the next generation of those technologies. “Atlas” is in recognition of our goal to serve as a bridge between our portfolio companies (primarily in the west) to the Middle East where the pace of capital deployment into industrial technologies is faster than ever before. Our encounters with global thought leaders at the Future Investment Initiative (FII), from Ray Dalio to H.R.H. Princess Reema Bint Bandar Al Saud, reinforced the message: we are at the cusp of a monumental shift.

In the spirit of bridging worlds and forging resilient futures, we spent the last two weeks deeply engaged with our LPs and portfolio company Transmutex (CEO Franklin Servan-Schreiber) in Saudi Arabia. Our journey started with the FII or what some call “Davos in the Desert”. Our goal was simple: make progress towards building an R&D facility in the region in line with our thesis on the need for nuclear energy as outlined in A Tale of Two Countries & The New Nuclear Future. Progress was clear, validating our thesis and justifying our return in the years to come.

At FII, we witnessed firsthand the synergy of public-private partnerships. For example, it was announced by NEOM Investment Fund CEO Majid Mufti, that NEOM's plans to purchase 25% of the global supply of steel at peak construction of the city. This further solidified our conviction in the importance of identifying a technology solution to vanadium price volatility, a critical mineral for turning iron into high tensile strength steel. The recent public announcement of the multi-billion dollar NEOM Investment Fund, demonstrates that if we can identify strategically aligned technologies, there will be large pools of equity and debt capital available to commercialize the technologies we invest in.

The Gulf is now ripe with opportunity for the next generation of industrialists and we are ready to position our companies to participate in this next industrial wave. This also coincides with a pendulum swing in the US investment landscape, from a focus on software dominant to hardware dominant companies with more durable moats – a return to the venture capital fundamentals of old. We are excited to lead this transition, to be at the forefront of this new era of investment, bringing together the best of the old with the vigor of the new.

— Theses & Commentary —

Investing in the Tailwinds of Public-Private Partnerships

Great venture investments are made on large tailwinds that last for a decade or more (as per Cameron’s mentor, Kevin Ryan). We see such a tailwind in the Saudi investment into industrial buildout and economic diversification away from oil. This is a tailwind that will see Saudi net manufacturing and technological exports grow, thereby necessitating an inflow of new industrial technologies. We sit at a unique moment in time when the world's most important player in global energy (the driver of economic growth) has decided to plough its vast financial resources via public-private partnerships into the diversification of its economy and the modernization of its state under a single banner, Saudi Vision 2030.

This initiative by Saudi Arabia has created one of the largest pools of public risk capital in history, $3.2T of which will be deployed by 2030. This capital will be directly invested in partnership with private entities towards the construction of new industrial facilities and technologies to diversify the Saudi economy .

Looking back on the history of public-private partnerships in the US, China, and Singapore, we have identified several key factors that lead us to believe in the potential for outsized impact from Saudi’s approach. However, the mere pursuit of these ambitious public goals supports our thesis of investing in resilience-enabling technologies. We believe we have identified a win-win-win for our companies (and others like them), Western allies, and the Kingdom. Just as the petrodollar served as a driving force in the global economy during the first phase of Saudi Industrialization (70s/80s), so will this new techno-industrial dollar serve as a driving force in the 2020s/2030s.

Singapore, despite having few oil reserves, is one of the world’s largest oil refiners at 1.5m barrels of oil per day. Public-private partnerships between state and foreign firms converted Jurong island (which were in fact a set of disparate islands) into an international petrochemicals hub. How did they achieve this? Calculated governmental coordination across key development areas. To attract foreign industrial companies, it wasn’t just a matter of co-investing – it involved long-term thinking about infrastructure, skilled workforce training, and subsidies / tax breaks of various kinds. This coordination across development authorities is a common theme in successful public-private partnership initiatives in pursuit of economic growth or diversification.

Silicon Valley’s emergence was in part from public-private partnerships in the form of research parks and industrial zones, and more importantly, a commitment by the Cold War DoD to buy Silicon chips and the products of private defense suppliers. This state demand-side component of industrial policy is easy to overlook because it was not emphasized in the industrial policies associated with the East-Asian which focused primarily on bolstering exports. The East-Asian strategy brings to mind currency devaluation, infrastructure investments, direct subsidies to strengthen industry in global markets, and advantageous trade arrangements. This strategy is in contrast to the state acting as an end consumer as was the case of the early Silicon Valley and US. Thus an effective approach to industrial policy often combines both coordination (as in Singapore) and the state promises to acquire goods (as in Silicon Valley). When these industrial policy goals and strategy is clearly and broadly communicated, positive outcomes can be achieved.

When looking at Saudi industrial policy, it has both hallmarks of strong coordinating authorities (like Singapore) and clearly articulate state drive demand (like Silicon Valley). In terms of coordinating authorities, Saudi has the state-owned Aramco, SABIC (petro-chemical manufacturing), and the Public Investment Fund (PIF). Aramco’s annual revenues are $400B and it has a market cap of $2.13T (making it larger than the combined market caps of almost all other significant oil majors). SABIC has an annual revenue of $53B (only BASF and DOW have larger revenues in the chemical sector, two companies that are the product of consolidation and historical state support). PIF has $700B in assets and explicitly functions like a development bank.

On the demand-side, the programs of Vision 2030 require huge amounts of material, technologies, and labor. The epitome of this is the $500B city development project of NEOM. It is not only a next-generation city, it is an industrial base. Even taking an extremely conservative outlook on the project, the scale of material, labor, and technologies to be used are of staggering quantities (as shown below). Despite external skepticism, construction on NEOM has already begun and it now serves as an open call for novel uses of construction technology and material manufacturing techniques. As per NEOM’s own reports:

- NEOM already has 3,000 + employees and 60,000 + construction workers

- $2B to be invested in the Port of NEOM , with the first advanced container terminal opening in 2025

- $6.1B raised to build the world’s largest Green Hydrogen plant at NEOM by 2026

- 85M tons of cement to build NEOM

McKinsey predicts that Saudi Arabia alone will spend at least $175B annually on construction over the coming years. This is projected to lead to shortages in domestically produced materials for the construction industry, unless local supply can be scaled up dramatically.

This state-driven demand component thus induces large CapEx investment into domestic production by ensuring a consistent end customer. This is the key accelerant to the rollout of industrial facilities that can be signed off with handshakes and offtake agreements, rather than only economic forecasts. This is also where the opportunity lies for venture investors. Identifying and addressing (via technology) these market dislocations that unlock project-financing capital for industrial companies aligned with these initiatives.

The Push Towards a More Resilient Economy

In one memo we shared on resilience, we stated that:

“In the realms of volatile industries and markets, resilience is the perennial strategy for the unseen and unpredictable adversaries that emerge from the highly interconnected world we live in today. It is not a one-off action but an integrated approach that combines foresight, preparation, fortification, and recovery. In a world characterized by constant flux, resilience is not just a protective shield; it's a competitive advantage.”

Saudi’s economic/industrial policies, articulated by Vision 2030, are best described as “state resiliencification.” This is distinct from “state developmentalism”, which better describes the industrial policies of countries like China and Korea. Developmentalism states that the best way for less developed economies to develop is through fostering a strong and varied internal market and imposing high tariffs on imported goods. This is not Saudi’s approach.

Saudi industrial policy seeks a rapid expansion of domestic manufacturing capacity and national economic sufficiency as per John Maynard Keynes’ definition in his 1933 essay National Self-Sufficiency. Keynes predicted a world where nations would be their own economic masters, capable of rejecting “interferences of the outside world” by localizing more of their production. We see this as a common theme throughout much of the world today, from Indonesia to the sprawling industrial policies of the United States. However in Saudi although certain industrial policies are closed loop (ie making local building materials for local construction), it is not isolationist. Saudi domestic manufacturing build out is predicated on collaboration with foreign companies.

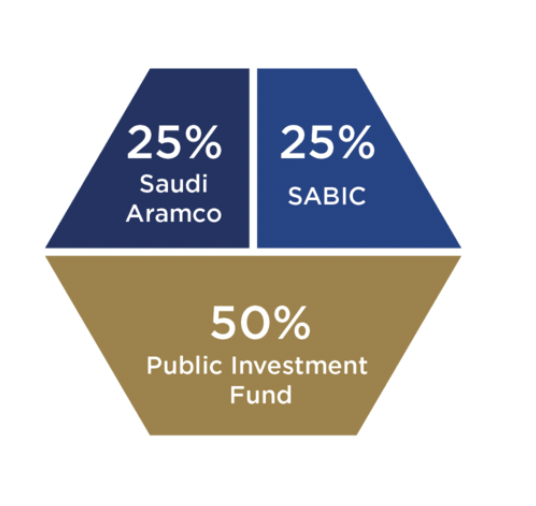

Positioning itself between “East” and “West,” Saudi Arabia is capable of collaborating with firms from around the world. While China and the United States butt heads, Saudi Arabia opportunistically works with the exceptional enterprises from both states. Industry bodies like Dussur, which collaboratively provide strategic incentives and co-financing for large-scale industrial projects, are attracting foreign companies that will increasingly onshore the production of petrochemicals and speciality metal products in Saudi. Dussur’s capital stack also demonstrates the desire to unlock coordination between public/private entities with 25% owned by Aramco, 25% by SABIC and 50% by the PIF.

Entities like Dussar are designed to induce foreign direct investment (FDI) in key sectors that does more than bring dollars into the economy. It also upskills the local workforce. This was successfully demonstrated in China in places like Shenzhen that has become a global center of excellence for hardware products. Well executed industrial policy creates a clustering effect – a positive flywheel where upskilled labor gain the skills to launch new local businesses that supply or compete with their foreign counterparts. We expect the same clustering effect to take place in Saudi in areas like NEOM.

In some cases, what venture capitalist Bill Janeway calls “productive bubbles” emerge. These are self-fulfilling speculative investments piqued by the state that can catalyze entire new industries (think railroads in 19th century America). If we look at American industrial policy today, it intentionally seeks to stoke private sector enthusiasm and attract capital to the climate tech sector and to commit to domestic production. Where climate takes an outsized role in the US policy, export diversification sits at the forefront of Saudi policy.

American industrial policy is more supply side focused than its Saudi counterpart. Support for businesses comes in the form of the IRA which provides loans (on the order of hundreds of billions of dollars), tax credits and grants. Buy American provisions for infrastructure projects or regulations like ITAR compliance are one way in which the American industrial base is provided demand side industrial policies, but this is not an integrated process.

The hybrid state / private actors are a core difference between American industrial policy and Saudi industrial policy. National champions certainly exist in America (Intel) but they are different in nature from companies like Aramco and SABIC, which are owned in large part by the state. This creates an altogether different “industrial policy coordination” picture to the United States. Saudi state and state-initiated projects provide concentrated, negotiable and accessible sources of demand for manufactured goods and technology firms that venture capital funds (like Steel Atlas) can capitalize on.

The Venture Opportunity of Investing in Moonshots with State Support

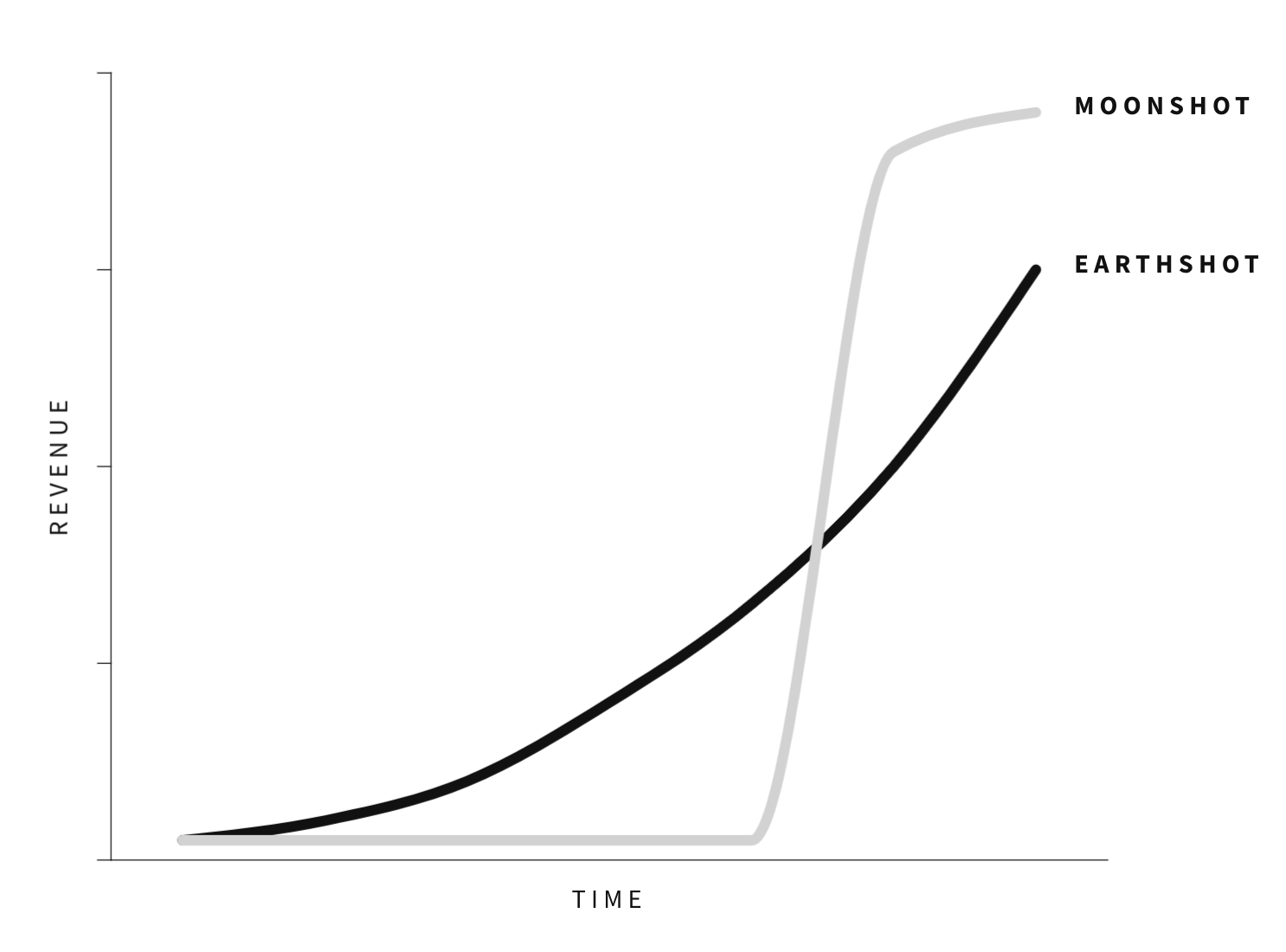

Public-private partnerships (like those occurring across sectors in Saudi) have the capacity to eliminate barriers associated with investing in businesses that require heavier CapEx and the construction of first of a kind facilities. Construction of these first of a kind facilities is one of the reasons people often say that hardware is hard, thereby implying that software is easy. There are many reasons that we disagree with this. It is neither clear software companies require less capital (Uber) or have higher margins (Wish, Blend, etc). However, building first of a kind facilities in particular can be quite difficult. This is what leads to the different growth curves we see in what we call earthshots and moonshots as outlined in our memo on the topic:

Once the first facility is built and clear technical requirements are met for product performance, adoption can scale quickly with efficient project-financing. This creates large and durable barriers to entry (because hardware is hard).

The public-private partnerships we see in Saudi can provide a massive tailwind for Moonshot investments by providing an accelerated path to commercialization. Like all markets and opportunities, being on the ground is imperative to capitalizing. We see a once-in–a-lifetime opportunity to quickly deploy resilience enabling technologies that will serve as the foundation for the coming industrial revolution in Saudi Arabia that can then be deployed across the US, Europe, and beyond.