Another request we have been receiving with increasing frequency from both our LPs and our founders is to learn more about Kevin Ryan, the Founder & CEO of AlleyCorp (one of, if not the top venture studio in the world). As LPs and friends of the fund, it is important for you to understand how we think about investing and growing early stage startups as well. With that, there is no individual that has influenced my (Cameron Porter, Co-Founder & General Partner) thinking than Kevin. So we have written a 7+ page memo on Kevin Ryan's Perspective on the Three Pillars of Company Building: Ideation, Hiring, and Fundraising.

We hope this memo serves as a window into the mind of the one the best. For context, after Cameron played professional soccer in MLS (the same league as Messi), he joined AlleyCorp as a team of 4 sitting out of MongoDB’s office. Kevin was not only his boss but a mentor as well. Beyond his immense professional success, Kevin is a kind, generous, and fun-loving individual. Another piece could (and deserves) to be written on all he has done to support me (Cameron) and those lucky enough to cross his path in life. (Thank you as always, Kevin!)

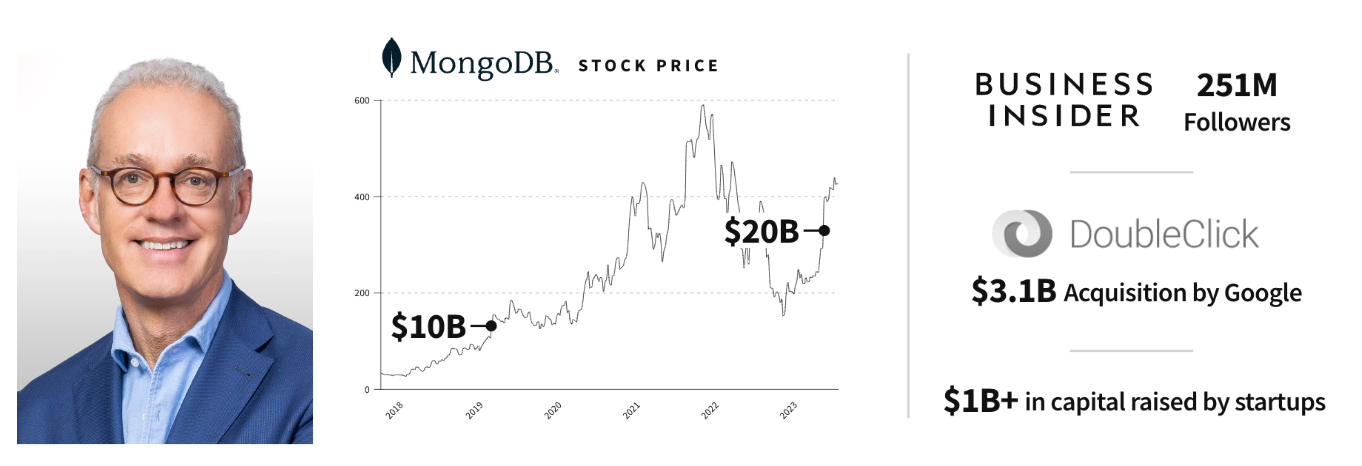

Often called the “Godfather of NYC Tech,” Kevin is a co-founder of MongoDB (NYSE:MDB), Business Insider, Gilt Groupe, Zola, and Nomad Health. He founds new companies with AlleyCorp every year. Earlier in his career, Kevin helped to grow DoubleClick first as President and then as CEO, leading their growth from a 20-person startup to a publicly traded global leader with over 1,500 employees, through IPO in 1998 and acquisition by Google in 2007. The companies Kevin has founded employ thousands of people and have raised well over $1B in venture capital along the way. We believe this gives his advice on ideation, hiring, and fundraising ample credibility.

Despite this track record, the internet has let Kevin’s thinking on ideation, hiring, and fundraising be buried in siloed interviews. We believe this is a disservice to us all in the entrepreneurial and tech community that this piece intends to remedy. Below are a few of our favorite pieces of wisdom from Kevin:

Ideation

Good ideas are all around you.

I’m always thinking about problems — what is too expensive, hard to get, or inaccessible? [video]

If you have a task that takes you more than 3 minutes to do online then there is an opportunity to start a business. [video]

When you see a market where people are making 40% profit margins, you have to think there is probably a better way. [video]

Whenever you have a question you want answered and you don’t know the site that will answer it — there is a company idea. [video]

Any time you see an area that is $50-$100 billion in purchases and there is not one site where you can figure out what you want to buy — especially in the B2B space — then that is where you want to launch a company. [video]

Focus on ideas supported by large tailwinds.

We like to make sure there is an obvious fundamental trend that can back us up for the next 5-10 years because when starting companies, we go with the assumption that we will be owning them 10-15 years later. [video]

You don’t need to be an expert to have good ideas.

Entire industries are being replaced by people outside of the industry. Most of the best internet ideas come from people who don’t have a background in what they are doing. [video]

Big market + No constraints

It has to be a big market so it’s interesting enough. It has to feel like there is a billion-dollar opportunity there. You’re not always going to get there but if it works, it’s that big. [podcast]

Is there a clear vision of the product that can be built? Is there a constraint? Is there some reason you can’t build this? [podcast]

There is always competition.

Any time I've started an idea, including Gilt, if it's any good at all, there are 20 people doing the same thing. [article]

Don’t focus on the financial models.

I never put together a financial model even though I’m a former CFO. I really have to just understand the consumer whether that’s a B2B or a consumer-consumer. I just have to understand what’s going through that person’s mind, what are the challenges, what are the problems. So it really involves a lot of interviews of people. [podcast]

Know when to discount feedback.

I threw the idea out to a couple of people, and some thought there were structural reasons why it would not work here, saying that France is a different market. And I just thought, "No, I think they're wrong. I think it's gonna work." [article]

Over-index on execution (aka people) not the idea.

The idea is not that valuable — what it is is execution. The idea only gives you a few months of extra time. [video]

When I think about starting a business, my view is that the idea itself is worth between zero and very little. Most new companies already have competitors when they launch and if they don’t, they soon will. [article]

Hiring

Don’t be an entrepreneur if you can’t hire.

You're going out and finding people yourself. If an entrepreneur comes to me and says they can't find a person or can't convince people to join, I would say, "Unfortunately, that's the job." If a salesperson can't sell, then you can't be successful. If you can't convince people to join you, you shouldn't be doing this because it's very hard. [article]

Always be hiring.

Your concept isn't worth that much, but if you can get a great team, then you'll be successful. So that's what I do all day long, I hire. I'm interviewing people all day long and retaining, making sure that our good people stay and are in the right spots. [article]

It’s about the people. Ideas are easy to get. What’s hard is if two people have the same idea. Whoever has the best team that moves the fastest and works well together wins. It’s about making the right decisions and tough decisions. [video]

Make sure hiring is the priority.

Kevin has two tests that he uses to decide if hiring is enough of a priority at a company outlined below.

Here’s a simple test: Ask the CEO if he or she spends more time on recruiting and managing people than on any other activity. For me, the answer has always been yes. [article]

Here’s another test of a company’s devotion to its talent: Is your head of HR one of the most important people in the company? I spend as much time with our head of HR as I do with our chief financial officer—and I have never considered having the head of HR report to anybody but the CEO. [article]

References are more important than interviews.

References matter most. It would be a great experiment to not interview people at all—to hire simply on the basis of the reference check—and see what happened. I’m pretty sure that most companies would make better hires if they did that. [article]

Below are some questions that Kevin recommends asking during a reference call:

Would you hire this person again?

If so, why and in what capacity? If not, why not?

How would you describe the candidate’s ability to innovate, manage, lead, deal with ambiguity, get things done, influence others?

What were some of the best things this person accomplished?

What could he or she have done better?

In what type of culture, environment, and role can you see this person excelling? In what type of role is he or she unlikely to be successful?

Would you describe the candidate as a leader, a strategist, an executor, a collaborator, a thinker, or something else? Can you give me some examples to support your description?

Do people enjoy working with the candidate, and would former coworkers want to work with him or her again? In what areas does the candidate need to improve? [article]

Fire fast.

In what follows, Kevin outlines how he would approach telling a low performer they are being fired.

You rank 10th out of 10 in performance. You’re probably great, but this may not be the right job for you. We may not be the right company for you. I know you don’t want to be in a situation where people think you’re the lowest performer.

Sometimes we can find a position in the company that is a better fit. Inevitably, the employee will question the judgment: “I’m not really the lowest performer.” Then I say, “Evaluating talent isn’t a precise science. But it’s very rare that multiple managers think you’re 10th out of 10 when you’re really number two. Maybe you’re number nine—maybe. But the real point is that I want you to be successful, and I don’t think this is the right situation or career path for you. [article]

B players hire C players.

The common assumption is that "B players" hire "C players" because they are afraid that hiring people as talented or better than them will reveal their weaknesses and threaten their position. Kevin challenges this belief.

B players hire C players not because they feel threatened by more-talented people but because most people don’t want to work for a mediocre boss. Think about it: Have you ever heard someone say, “I just got offered a job. The person I’ll be working for isn’t very impressive, but I’m going to take it anyway”? That’s not something talented people generally do. [article]

Good hires finish things.

I think, too, that the hardest quality to find in a new hire is the ability to bring things to closure. Some people don’t realize that analysis is useful only if it results in a decision and implementation [article]

Fundraising

As the opening quote alluded to, if you have a good idea and a great team, the money should follow. However, there are a few tactics you can follow to optimize your fundraise.

Start raising before you start raising.

When I plan to be raising in six months, I’m already out there, proactively connecting with VCs, having coffees, making as many of them aware of my company as possible The conversation is safer when I’m not raising money. [article]

Hone your pitch with friendlies and poor fits.

I like to have one or two meetings with either VCs that might not be the ideal fit or angels or other people who can give me commentary on the idea and how I’m presenting it. [article]

Exude confidence and know your numbers.

Kevin recognizes VCs have biases based on things you cannot control when you are going to out fundraise – having gone to a particular school, having had a particular job, etc. However, VCs have biases that you can control.

There are two you can control: a bias toward founders who know their numbers backward and forward, and bias toward founders who exude confidence in every interaction. With practice, you can make sure you hit the mark on both. It requires a lot of arduous and uncomfortable rehearsal, memorization and rounds of feedback, but it’s well worth it. [article]

Here’s a micro example — I was in a VC meeting, and someone asked, ‘What do you think the commission structure will be next year?’ the CEO I was working with said, ‘I can’t remember the exact number. Let me get back to you.’ Once in a while, you have to give this answer, but it’s a terrible answer. I stepped in and said, ‘Between 15 and 20%, but it’ll get better over time. [article]

Give VCs schmuck insurance.

Never tell them who, but do say that there are other people at the table. It’s simple really. A competitive round is better because that means more people are interested. People feel like they have schmuck insurance when they think other people like the company. [article]

At some point in your raise, you might remind firms you’re speaking to that you’re going to the other coast — San Francisco or New York, depending on where you are — on Monday, a way to signal that you’re going to a partner meeting without being obnoxious and bringing it up directly. Everyone will understand what you’re saying. [article]

Make VCs feel special.

VCs are just like everyone else in the world. They want to be wanted. They need to feel like they bring value and that very smart people (i.e. you) realize and appreciate that. “When a VC feels this, they feel more invested in you. [article]

You want a VC to think, ‘I know there are other people interested, but I have a great relationship with the CEO. I think she really likes me and the firm and I have a good chance of winning that deal.’ You want all the VCs you’re talking with to feel this level of comfort. You need to make it clear you value the services, tools, resources that they bring to the table, and that you’ve been hearing good things about them in the market. [article]

Run an auction not a raise.

When I want to raise $5M or $6M, I go out and I say I want to raise $3-5M. I believe in the auction strategy. There’s nothing that makes people feel better than when you go back to [the VCs] in two weeks and say, ‘Actually, I know I said $3-5M, but it’s really going to be $5-6M.’ That means other people are interested. [article]

Your goal in this process is singular: get as many term sheets as you can — not 50, but two, three, four. [article]

Some founders may feel guilty about this process of asking for money in an auction, but Kevin reminds founders of the following:

What you’re doing is giving [VCs] an opportunity — a chance to be a part of a company that’s going to change an industry. [article]

Being #1 compounds.

I'm always pushing as hard as possible to be that number one player. You get all the PR, which is self-reinforcing. No one writes about number two. People want to work for the leaders — so do vendors and investors. It's about being there and going really aggressively in the beginning. I always end up raising more money than my competitors, spending more, hiring more people and hiring them faster to make sure that we win. [article]

Set firm deadlines.

You should do two weeks of meetings with VCs and ask for term sheets four weeks later. [podcast]

The right time frame between the final meeting and term sheet is typically three to four weeks. That gives VCs the time they need to get their ducks in a row, but not more. Be clear and specific about your deadline — give people the exact date when term sheets are due. [article]

You need to give VCs enough time but not too much time. Let’s say I told you that you’re back in college and there’s a paper you can write to win $10,000 but it’s due in six hours. You’re not going to work on it. If I told you it’s due in four months, you’re not going to work on it. If I told you it’s due in five days, you’d say, ‘Yeah, I can do that. [article]

Choosing which VC to work with.

What follows is relevant after you have gone through the process of meeting with VCs and have multiple term sheets in hand.

For most [VC] firms — with a few exceptions — you will seldom see anyone other than your point partner. So you’re not getting a firm, you’re getting a person. You need to feel good about that person. [article]

In the situation that you have a firm/person that you would prefer to work with, Kevin lays out a rough rule thumb for deciding if you should go with them – even if they don't give you the best terms. Within 5% [of the valuation] it doesn’t matter. At 10%, I still want to choose the right person. At 30%, I’m not going to go with someone that I like more. That’s too much for me to give up. [article]

If you’re raising your first round of funding, it’s always more valuable to have VCs that are local. For your second and third rounds, you can go elsewhere. It’s less important. [article]