Last week, I sat down with a man that could no longer see the light at the end of the tunnel. It was a 30 minute catchup with a growth investor you would all know. Archetypal in many ways, this investor had (rightly) spent his career (making lots of money) investing in the software that has been eating the world. But, the release of Anthropic’s Mythos in particular had fully shrouded his North Star. He met with me hoping to gain faith in a new light.

His questions were more like pleas to (finally and fully) invert his view of what is “investable”. He wanted to believe in hardware like we do. He wanted to know there is a bastion of defensibility in an age of epic AI.

So I gave him two answers to help him find light again — one he expected and one he did not. I’ll give you both and what they (+ this broad market reorientation) mean for our fund.

The Expected Answer (Hardware)

Seven of our ten Fund I companies could be rightly viewed as “hardware companies”. But they come in different flavors. Some build large capex heavy facilities to deliver needed commodities (eg Valar Atomics). Some sell critical system components across hard asset businesses (eg Autonymy). Some even sell software but that software is hydrated with proprietary data from large scale sensor deployments (eg GenLogs). So why are all of these hardware companies “venture backable”?

We think its best to view a venture backable business as a black box with a few key characteristics:

1/ Can produce large, defensible cash flows.

2/ Cannot fund development and delivery with cash flows.

3/ With access to capital can accrue value and command liquidity fast.

Notably, none of the above criteria exclude hardware. In fact, we believe they can even favor hardware companies. However, the most common forms of push back are (1) due to the assumption of relative margins of hardware vs software, (2) due to higher R&D + capex costs of hardware vs software and (3) due to slowness to market of hardware vs software. However, all of these concerns are demonstrably false or misunderstandings of what the market actually cares about.

1/ On relative margins → simply put, category-winning companies (software or hardware) have great margins. On operating margin, the metric that actually measures business quality, hardware often beats the top of the software stack. Nvidia ran a 73.6% gross and 66% operating margin in Q3 FY26. TSMC posted 59% gross and 49% operating in 2024. ASML clears 51% gross and 33% operating selling the most capital-intensive machines on Earth. Apple ran 47% gross and 32% operating in FY25. And if you think this is a phenomenon limited to premium tech-hardware, Saudi Aramco — selling the most fungible commodity in the world — generated $480B of revenue in 2024 at 54.5% gross and 43% operating margins. Compare that to the ten largest public software companies (Alphabet, Microsoft, Meta, Oracle, Palantir, SAP, Salesforce, AppLovin, Shopify, Intuit), which post a median GAAP operating margin of 30%. Hardware produces durable margins across categories (chips, fabs, capital equipment, consumer hardware, commodities).

Software's COGS look thin (hosting, support), which inflates gross margins, but the real cost of running a software business sits below the gross line. Sales and marketing typically runs 30 to 50% of revenue at scale (Salesforce spent 35% of revenue on S&M in FY25, Snowflake 48%), and R&D is expensed as opex rather than capitalized, compounding the drag. Hardware companies, by contrast, embed most of their cost of doing business in COGS (materials, fab utilization, components) leaving operating margin closer to gross margin. A software company converting 75% gross to 25% operating is bleeding 50 points to CAC and R&D opex. A hardware company converting 50% gross to 40% operating is keeping nearly everything it earns.

2/ On higher R&D + capex → back to the black box. The market does not care what you spend your money on. It only cares about the terminal value of free cash flows that spending generates. Where a Valar Atomics may spend billions in equity on facility down payments, an Uber spends on sales and marketing. Both produce defensible free cash flow. Whether it is R&D or S&M or any other combination of letters, the market does not care as long as the result is lots of free cash flow.

3/ On slowness to market → yes, in many cases bringing a hardware product to market takes longer. GenLogs had to build and install hundreds of sensors across the US highway system before they could start ramping sales aggressively. That just takes time. A pure play, supply chain software company (we can call them “Freeway”) could just start selling into that market generating revenue. But once again, revenue today (although correlated with value) is not determinate of value. The value of a company is the sum of all perceived probability weighted and discounted future cash flows. It could very well be the case that the mere installation of the GenLogs sensors increases the probability of future cash flows more than incremental revenue today does for the software only Freeway. Slowness to revenue is not slowness to value. This is arguably most clear in drug development where the trial stage determines value ahead of a single sale. The same phenomenon is occurring in the nuclear reactor market where finalized designs, safety certification, and site selection are determinant of value ahead of revenues.

—

What should be most compelling about the above is that hardware has been and remains an attractive category of investment for venture capital even if it gets more competitive as more investors (like our growth investor friend) start to play in the hardware sandbox. Although valuations may be rising due to increased competition, this increased competition also signals increased access to capital. As funds get more comfortable pricing hardware risk / adoption / deployment timelines (ie develop more robust underwriting methods like they have for SaaS), prices will also increase due to perceived lower uncertainty (even if the quality of the company has not gone up).

The irony of this AI driven migration from software to hardware is that it embodies the same type of dogmatic groupthink that ensures the existence of great opportunities at good prices. Just as the dogma of the day told investors to avoid hardware, now the dogma tells them to avoid software. And we think that is exactly wrong.

The Unexpected Answer (Software)

When we hear dogma, we smell an opportunity. As the venture market is dogmatically turning away from software, we are even more bullish on it. In fact, our first investment (to be announced soon) out of Fund II is software. Pure, sexy, unadulterated software. In fact, I am even willing to bet a higher percentage of Fund II will be software than Fund I. Why is that?

Investing in hardware teaches you important lessons. You can probably learn them investing in software too but somehow they are just more legible when you are dealing with the “real” world.

1/ Reality is really fiddly → if you have not read John Salvatier’s 2017 blog Reality has a Surprising Amount of Detail, now is the time. If you don’t have the time, John describes the process of building a staircase and how many little details need to be figured out at each step. He concludes:

It’s tempting to think ‘So what?’ and dismiss these details as incidental or specific to stair carpentry. And they are specific to stair carpentry; that’s what makes them details. But the existence of a surprising number of meaningful details is not specific to stairs. Surprising detail is a near universal property of getting up close and personal with reality.

You can see this everywhere if you look. For example, you’ve probably had the experience of doing something for the first time, maybe growing vegetables or using a Haskell package for the first time, and being frustrated by how many annoying snags there were. Then you got more practice and then you told yourself ‘man, it was so simple all along, I don’t know why I had so much trouble’. We run into a fundamental property of the universe and mistake it for a personal failing.

Investing in hardware, you get to see teams of exceptionally smart people smash into the fiddliness of reality over and over and over and over again. There are so many ways to build so many seemingly obvious things. One fascinating example of this is how during WWII the US military forced its allies to converge on screw threading. Everyone had different screw threading for different reasons (available tooling / application optimization / performance etc). But many screw threadings meant that nothing worked together. So the US military mandated convergence. This constraint (like all good constraints) allowed everyone to move forward with other fiddles faster.

2/ Speed really matters → it all boils down to learning rate. The faster you build something the faster you learn and thus the faster you can move forward. Speed compounds because learnings build on each other. SpaceX's advantage over the competition is not linear with how many more rockets it has launched than its competition. It’s exponential. Every future rocket integrates and benefits from prior rockets.

Once learnings are incorporated into designs, they function as guardrails that accelerate the path to future (and more nuanced) learnings. People do not need to rehash solved problems.

What is Software

To demonstrate why these two lessons mean software will capture more value in the age of AI, we need to define what software is.

Software encodes standardized patterns of thought. Great software encodes patterns that (a) expedite the delivery of value, (b) eliminate mistakes, (c) enable mass coordination. Software (as opposed to AI) is deterministic. If two people put in the same input, they both get the same output. No “creativity” (or non-determinism).

Another way to put the above is that software is a set of common constraints. Much like the screw threading, these constraints allow more to be done more efficiently. People are not “solving” the same problem over and over again. And their solutions are coherent, i.e. they build on one another. Software thus allows more people (intelligences) to act more efficiently towards common goals. People (intelligences) don’t waste time doing things they shouldn’t. Doing so is costly in terms of time and money.

Software is thus valuable because it saves us time and money in the achievement of specific goals. Great software does this by having discovered and encoded all the latent fiddliness in digital processes.

Why does Microsoft Word have so many complicated features? What about Salesforce? Or AWS? It’s because they have dug deep into the crevasses of reality and smoothed out the sharp corners we would all eventually discover. They are just the most complex because they have gone the farthest. These software products have compounded on their learnings over and over again to build better and better guardrails for intelligent people trying to achieve specific outcomes as efficiently as possible.

Why AI Makes Software More Valuable

AI models are expensive to build and run. NVIDIA is the most valuable company in the world because their systems currently result in the lowest watts per token. Minimizing the cost of leveraging AI models is big business. But lowering the energy cost per token is only one way to do it.

Good old fashioned deterministic software is another. Just as software provides the guardrails to ensure the efficient and effective application of generalized human intelligence, so too will it provide the guardrails to generalized agentic intelligences. Traditional SaaS type solutions will ensure that agents do what you want the way you want it — not wasting time/tokens on standardizable chains of reasoning and ensuring reliability in performance. In so far as SaaS like systems will be used to coordinate arbitrarily large numbers of agents, the value of these systems will increase proportionally assuming usage based pricing (or token cost plus).

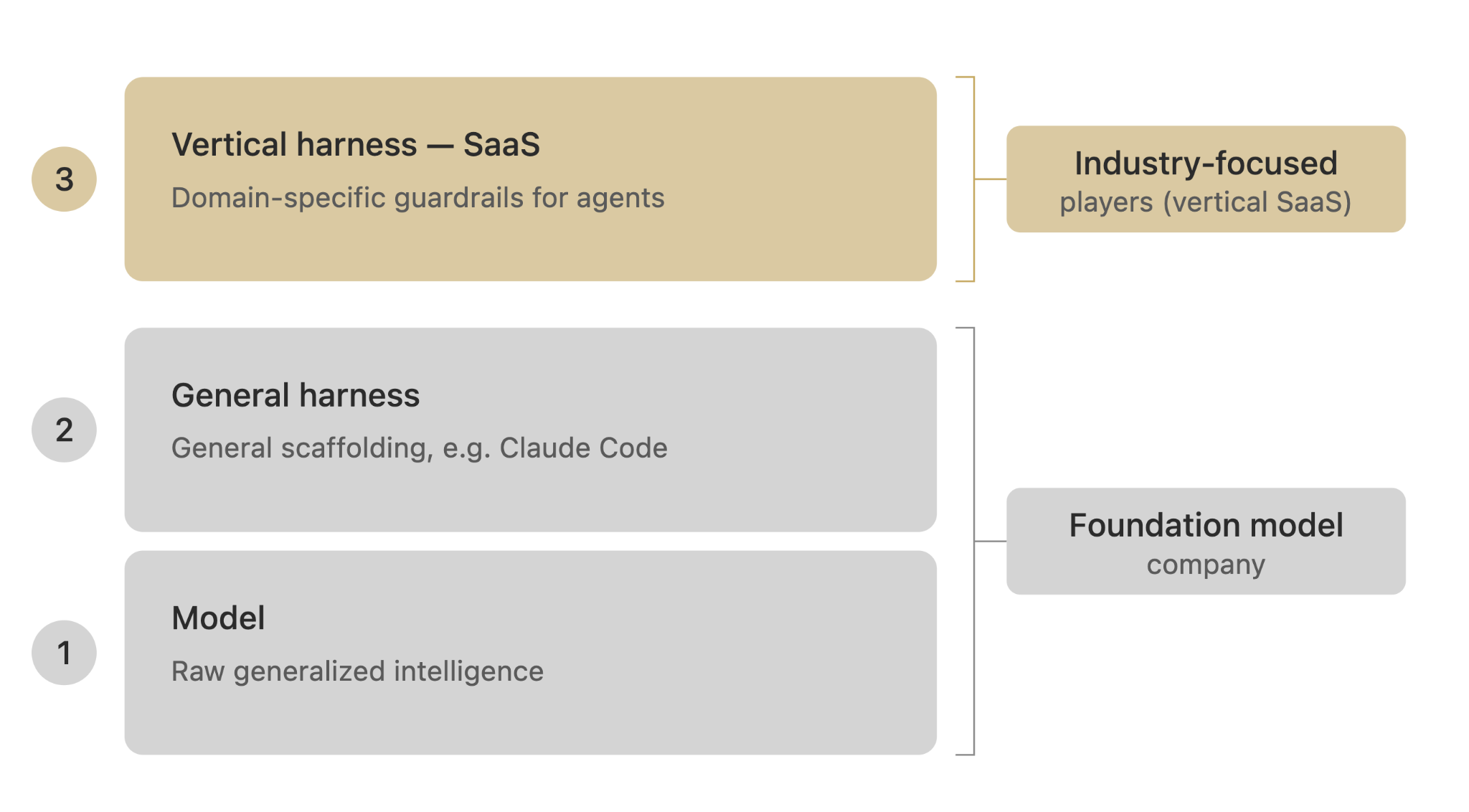

We believe the value of the “harnesses” layer for foundation model companies is the canary in the coal mine. What made Opus 4.5 so compelling was not the model but the Claude Code harness that unleashed the models capability by providing the appropriate set of guardrails. Over time, model performance is unlikely to be the only thing that matters. Rather differentiation will be found through the combination of (1) model + (2) (general) harness + (3) (vertical) harness. (1) and (2) will be provided by a foundation model company. We expect (3) to be provided by industry focused players aka vertical SaaS players.

Why Software Companies Will Win (Again)

In February, “SaaSmageddon” wiped out over $1T in SaaS market cap. This was driven by the belief that with sufficiently powerful models and agents (1) code complexity was no longer a moat (2) migration was no longer costly. Based on these, it was assumed that the model companies would durably take share from SaaS companies by either (a) directly providing systems to customers like Claude Code or (b) indirectly enabling customers to build their own solutions.

Yes, software companies will need to reorient and re-architect (as we will discuss next) for an agentic future justifying intermediate uncertainty in the market. However, we believe the terminal value of those that do will be greater than ever before because their systems stand to be leveraged more than ever before. Their true moat was never code complexity or switching costs. Just like hardware, we believe it’s their speed and understanding of the fiddliness of reality.

Enabled by coding agents, software will move faster than ever before. The constraint though will not be code complexity but rather the total dollars a company can invest in agents. What will constrain those agents is a deep understanding of the problems they are attempting to solve. Companies, software or hardware, will need to uncover the surprising amount of reality hidden in every problem there is to solve for organizations. Those that do a better job of understanding that ever expanding taxonomy will win.

The More Problems You Solve ... The More Problems You Can Solve

Counterintuitively to some, we believe that the coding capacity unlocked by agents will lead to further differentiation faster. The best software companies will move faster forward in the right direction than ever before. Small deviations in early direction are exacerbated not eliminated by speed. AI will thus accelerate early differentiation. And because learnings compound, software winners will be able to compound on that advantage faster than ever before. Within any problem, there is an infinite runway for improvement. As Bezos likes to say, the customer is perennially dissatisfied.

Thus, we believe as long as intelligence (agentic or human) has a marginal cost, the best deterministic software companies will be valuable. They will ensure organizations and individuals get the most out of their precious token budgets. Although there will be losers who fail to adapt to this new future, we see a future where the model companies and the “SaaS” winners are bigger than ever before. More intelligence (enabled by the mass deployment of agents), better directed (with software), will grow markets.

And we see many reasons why the foundation model companies will be unable and unwilling to change that to “capture it all”.

1/ Informational Constraints → as demonstrated by capitalism, knowing all the right problems to solve and how to solve them is best achieved via decentralization vs centralization.

2/ Operational Constraints → the deployment of agentic systems is hard and likely requires specialists in specific domains. The launch of the Deployment Company by OpenAI is evidence of this along with the success of Palantir and their iconic forward deployed engineer.

3/ Political Constraints → even if (1) and (2) do not hold, there may be a strong political incentive for the model companies to nurture a vibrant ecosystem on top of their capabilities instead of eating it all. Being deemed a monopoly is risky.

On Software Architectures

To be among the next generation of software winners though will require companies to re-architect their systems around a new set of axioms. Which, when combined with what we believe is long term durability of deterministic software, makes investing in this area incredibly exciting again.

1/ Intelligence is only constrained by capital → software systems will need robust ways to flexibly allocate capital towards tasks, track ROI, and respond to large variances in spend day to day. If your systems cannot answer what you return on token spend is, it will be replaced with one that can.

2/ Systems will have to handle arbitrary large numbers of “users” → software systems were used by a relatively stable and finite number of human users. Not only will systems need to respond to fluctuating user/agent counts based on token budgets, they will need a new identity layer. This layer will need to distinguish between human and agent users. Agent users will need to identify attributes that tie them to the permissions of human supervisors. Human supervisors will need ways to scalably permission actions and review deviations from expected performance.

3/ Systems will evolve as fast as problems can be uncovered → to enable this flexibility we expect systems to be designed around fully event driven architectures. These event databases will be the ultimate source of truth from which arbitrary API and UIs will be constructed on the fly as companies uncover problems for their customer base.

The Implications for Industrials

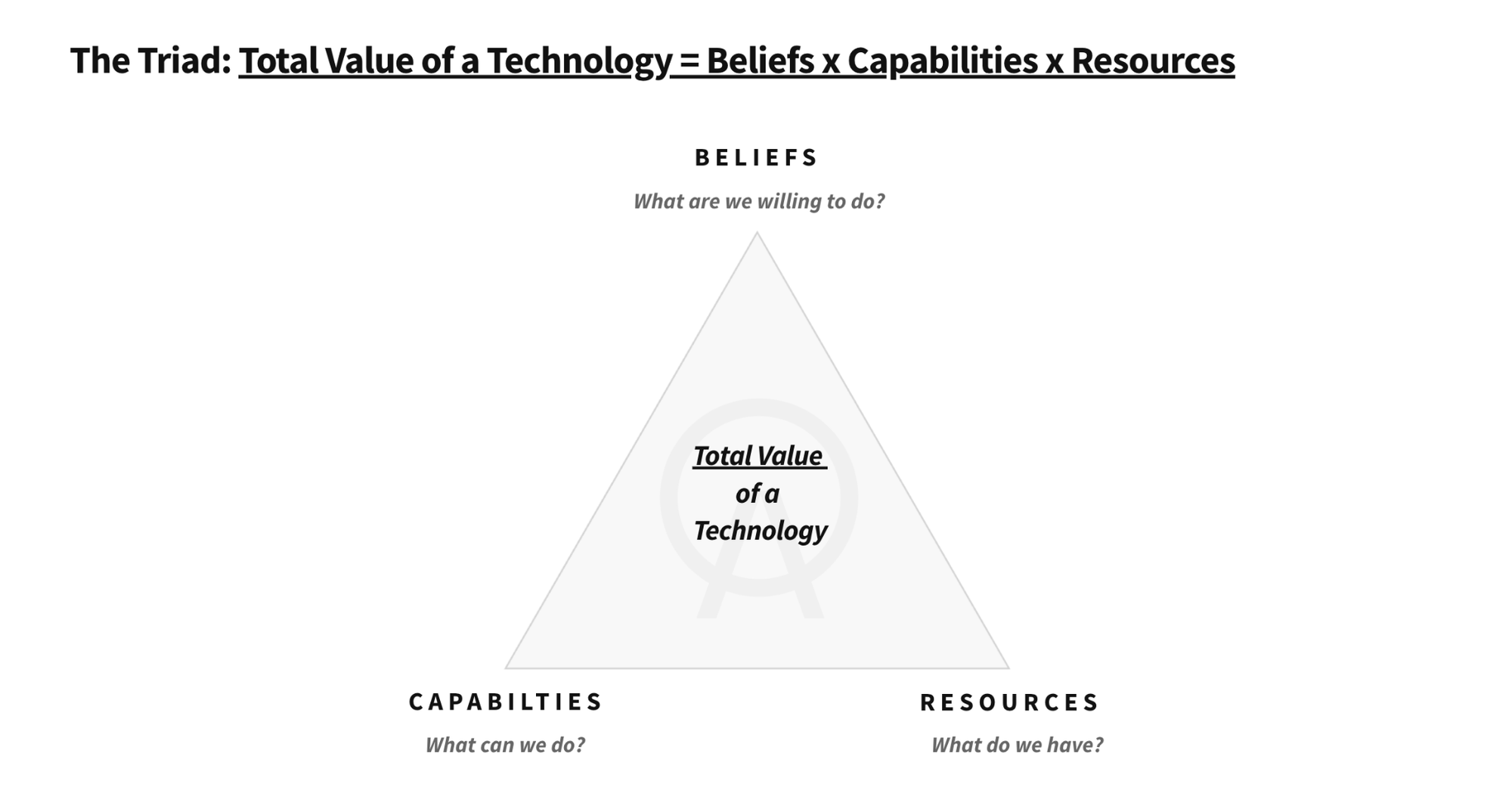

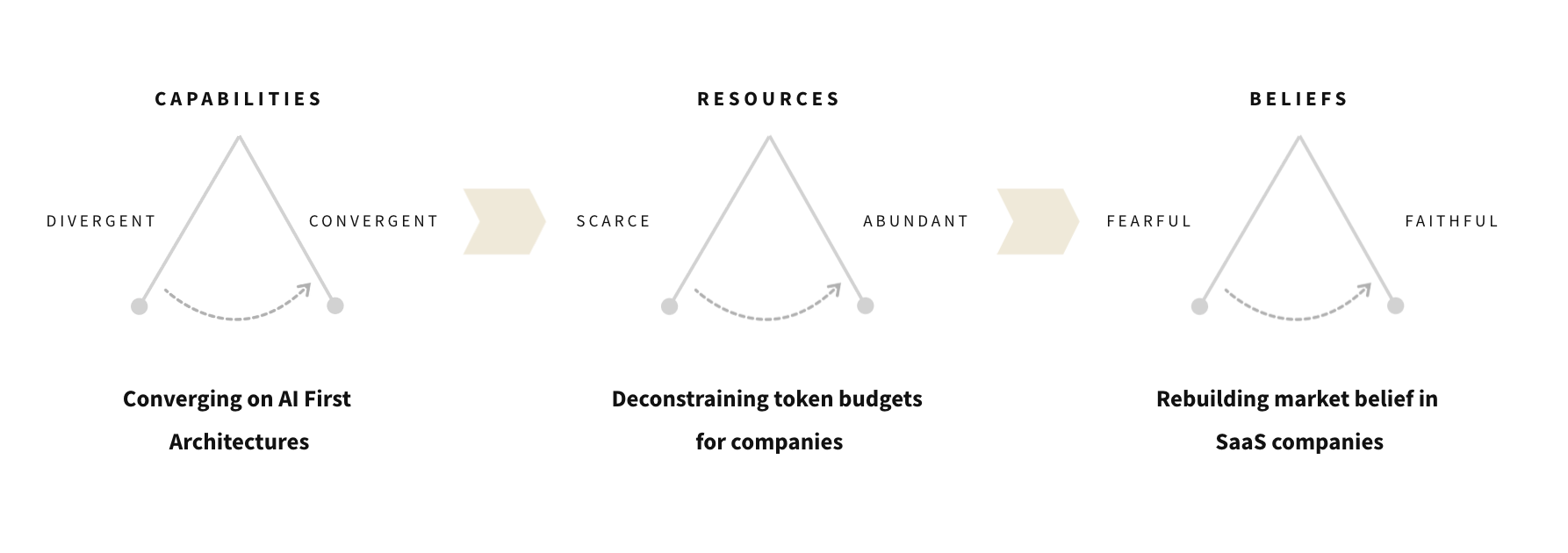

Ultimately, the desire to lean into the software stack that will power the future of industrials is, as always, grounded in our investing framework called the Triad (deep dive here). The short version it is that the best investment opportunities emerge when the market’s belief about a technology has the potential to move from fearful to faithful (AI will kill SaaS → SaaS will enable AI) because that technology can turn a scarce resources (tokens) into more abundant one and do so at a moment when the market is converging on a form factor (the agent/AI first architecture) for a given capability. When this happens value accrues quickly to companies at the vanguard of the market re-orientation.

Across our Fund I portfolio, we have already seen this pattern play out. Valar Atomics is deconstraining energy for industrials/data centers (scarcity → abundance) using a modular nuclear reactor design and quickly capturing value as the market has moved from fearful to faithful about the future of nuclear deployments. GenLogs is doing the same with freight capacity. Framework Automation with American made textiles.

We are excited to continue to use our unique access to leading global industrial companies and fast growing startups to identify and invest behind the next generation of software solutions. Software solutions that understand their role in providing the guardrails that ensure maximal value from scarce token budgets and are built with a new set of architectural primitives in mind. These startups will enable industrial companies that care about reliability above all else to finally capture value from the capabilities enabled by the foundation models. After all, it is Finally the Long Beginning of AI.