The purpose of Steel Atlas is to invest in the technologies that will enable economic resilience across the value stack. We believe we are living in an increasingly volatile world and therefore the companies deploying resilience-enabling technologies will generate outsized returns.

Going forward, each of these updates will provide you with an inside look at how we use this thesis to navigate the venture capital landscape while keeping you informed about the portfolio performance and exposing you to the companies we are currently evaluating.

At the risk of oversimplification, there are two driving forces that have led to more volatility across core sectors of our economy – interconnectivity and fragility. Interconnectivity has increased as a result of globalization (supply chains, communications networks, financial infrastructure). Fragility has increased as a result of declining interest rates since the 1980s. Declining interest rates incentivizes investment in growth at all costs and efficiency over capacity. This leads to fragile systems. Highly interconnected, fragile systems are vulnerable to cascading shocks, otherwise known as volatility.

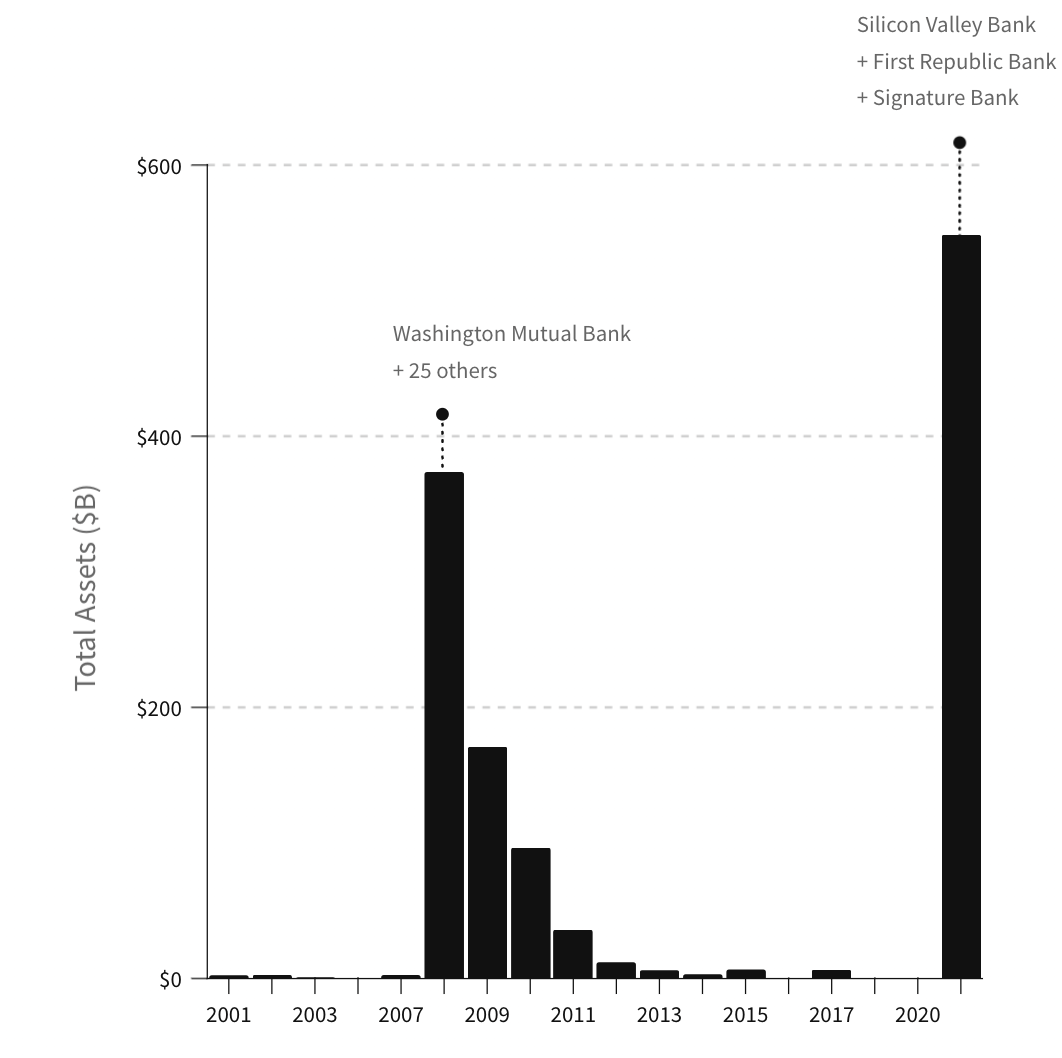

Examples of volatility from highly interconnected, fragile systems include the most recent banking crises in the US and German energy prices during the Ukraine war. We will explore the latter further to demonstrate how the existence of these volatility shocks can be used to post-facto identify compelling investments opportunities. We can then contrast this method with an a-priori approach whereby we look for leading indicators of volatility, notably supply concentration.

Post-Facto Sourcing

Of the two methods, post-facto sourcing is the simpler one. By tracking the news, we can identify volatility shocks. However, this increased legibility of the problem leads to higher competition between companies that address the volatility shock as well as more investors looking to fund said companies.

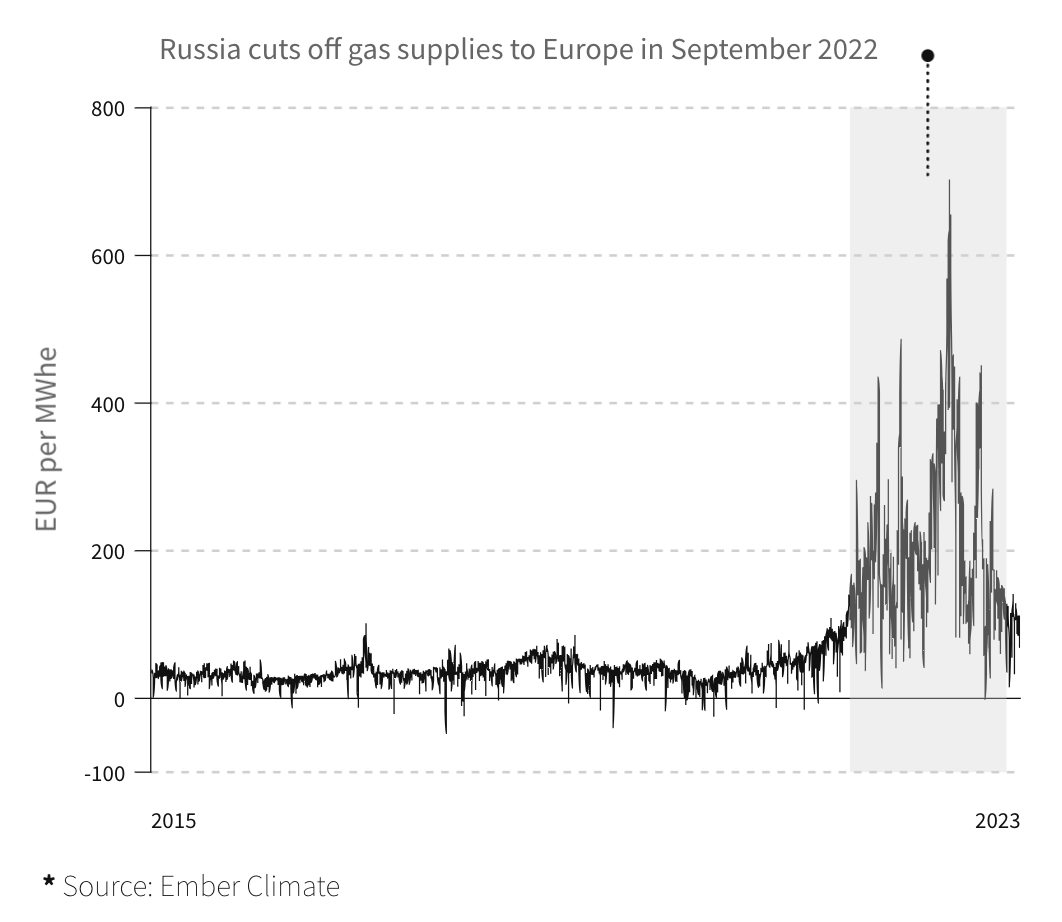

One sector where this dynamic has clearly played out is energy, in particular as it relates to baseload power in Germany. Since the 2000 Renewable Energy Act, Germany has been a pioneer in green legislation. The 2002 Nuclear Exit Law set the stage for phasing out nuclear power by 2022. Germany's "Energiewende" policy, beginning in 2010, significantly increased renewable energy investments, making it a world leader in renewables by 2022.

However, renewables like wind and solar provide intermittent energy supply. Without (currently non-existent) grid scale energy storage solutions, Germany was heavily reliant on non-nuclear baseload power solutions, in particular natural gas from Russia’s state-owned energy company, Gazprom. This concentrated reliance on Russia, left Germany vulnerable.

In February, 2022, Russia invaded Ukraine. Seven months later, Russia cut natural gas flow to Germany by half to just 20% of capacity. This triggered a more than 10x increase in energy prices.

As the energy crisis in Germany unfolds, it has become abundantly clear that their lack of reliable, domestic baseload power is a massive risk to their economy. It is no longer tenable to move forward with shutting down their remaining nuclear reactors.

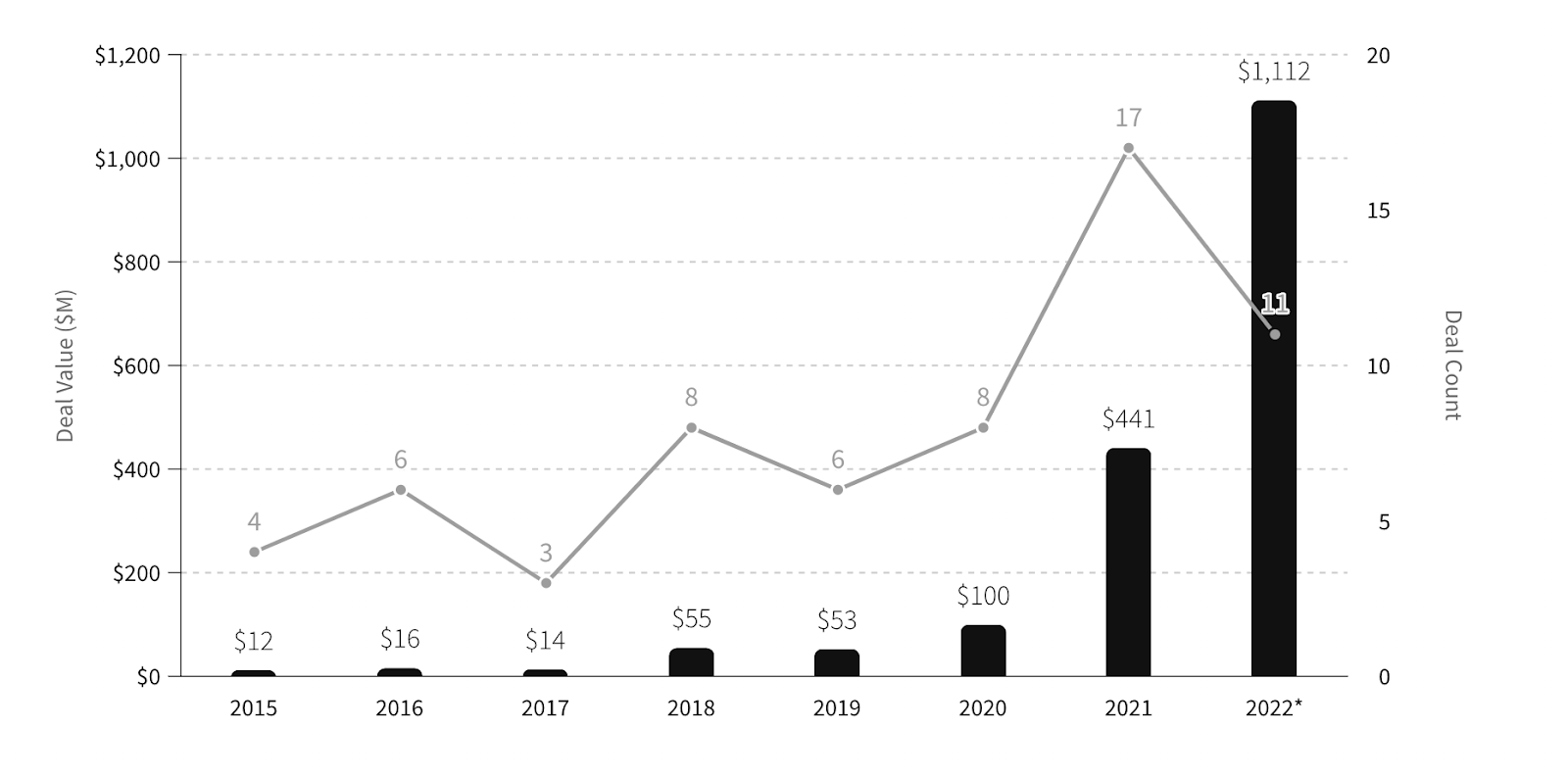

This is forcing individuals and institutions in Germany and around the world to reevaluate nuclear fission as a viable path to energy independence via clean, reliable baseload power. In 2022, over $1B in venture capital flowed into nuclear technologies.

With this in mind, we have been working closely with companies like Transmutex (backed by Union Square Ventures and AlleyCorp), who have designed a subcritical reactor that converts the waste generated by existing light-water reactors to energy. Their approach reduces certification and operational costs, addresses nuclear fissions core political concerns of safety and waste, setting a path towards abundant clean electricity.

The opportunity is not limited to nuclear fission and fusion though. With the US passing legislation like the Bipartisan Infrastructure Law that provides $97B in funding for clean energy research, development, demonstration, and deployment, there are massive capital tailwinds supporting the sector. Led by engineers from SpaceX, Arbor Energy is capitalizing on this by building modular power stations fueled by organic waste. We share more details on Arbor in our Deals section below.

Although it is the early days, we are already seeing the value of our thesis driven approach as it relates to post-facto sourcing. Founders and other funds will increasingly recognize us as the resilience fund. This identity and expertise will generate a more qualified top of the funnel and ultimately aid us in winning allocations in the most competitive deals. Arbor Energy is a great example of this already taking place.

Going forward, you can expect us to keep our ears to the ground for emerging volatility across the core sectors of our economy, from the supply chain to the energy transition and built environment. However, we will complement this reactionary approach with a proactive sourcing method predicated on a-priori vulnerability analyses.

A-Priori Sourcing

Energy was not the only sector of the economy affected by the war in Ukraine. Russia is one of the largest producers of nickel in the world. Nickel is a core component of the cathodes in lithium-ion batteries, the batteries that power EVs. We believe this foreshadows what will become an increasingly volatile supply chain if the industry continues on its current path. With the International Energy Agency estimating a 42x increase in demand for lithium alone by 2040 due to batteries, the opportunity for alternatives is growing exponentially.

So why are we betting on future volatility in batteries? Within any sector, we believe that there are specific characteristics that we can use to measure vulnerability to volatility or inversely a lack of resilience.

Volatility Vulnerability = Risk / Resilience

Risk = [probability of an event] x [value of exposed human & economic variables]

We view the overall risk as the integrated value of the sum of individual risks at any given time. This overall risk is a measure of opportunity size because it factors in the total potential value of exposed human and economic variables. (Thank you to our advisor, Greg van der Vink Ph.D for providing us with this quantitative framing.)

Total Risk = ∫ [Σ (probability of event) x Σ(value of exposed human & economic variables)]

With this framework, we can begin to predict opportunities for investment by identifying sectors where we see increasing probabilities of events and increasing value of exposed elements. Although there are many common patterns we can use to identify increasing probability of an event, the one we will focus on with batteries is supply concentration. Sizing the value of exposed elements can follow the bottom-up methods of market sizing often used by venture capital firms. The key is identifying long-term growth trends across both.

Based on our framework, the battery industry has high total risk and thus represents a massive opportunity for investment. The probability of a volatility inducing event is high because the supply chain is highly concentrated. Congolese mines are responsible for 70% of the global supply of cobalt, a key component of lithium-ion batteries. There are also increasing reports of human rights abuses at these mines. Furthermore, China controls 68% of global nickel refining and 73% of cobalt. Lithium mines in Chile and Peru risk nationalization due to political instability.

As we already noted at the beginning of this section, the battery market (or as we would call it exposed elements) is large (~$35B+) and growing (~15% CAGR). In the US, the passage of the Inflation Reduction Act generated further tailwinds by providing supply and demand support for domestic batteries. EVs with batteries made from components in the US or its allies are eligible for $7.5K credit. The battery supply chain is supported by credits for 10% the cost of making battery minerals and $35 per KWh of battery cell capacity produced.

This a-priori analysis has led us to look for companies building new batteries that do not rely on the materials that further increase the risk of concentrating the supply chain. As the risk of volatility increases (or volatility materializes), we expect these companies to see accelerated value accrual that will disproportionately benefit early stage investors like us.

Group1 fits our criteria. Led by a second-time founder in the battery space and based on IP developed by the inventor of the lithium-ion battery, Group1 is developing the materials to unlock potassium-ion batteries – an alternative that avoids the supply concentration risks noted above while meeting performance criteria demanded by the industry.

Ultimately resilience is about building a more balanced world. Whether it's the materials we use, where we get them, or how we trade-off short-term needs vs long-term consequences, balance is key. We could not be more humbled to be making investments that we believe will generate exceptional returns, while making the world a more balanced place.